Strengths

- The best-performing precious metal for the past week was silver, up 5.38%, about twice the price gain of gold. China bought 160K ounces of gold in March, the largest amount since February 2025 and as much as it purchased in total over the past five months. The country’s total holdings now stand at 74.38M ounces and are worth almost $350B at current gold prices, according to Canaccord.

- According to Scotia, at $4,700/ounce gold, the weighted average ROIC for gold companies for 2026, 2027, and 2028 is 24.9%, 21.9%, and 19.7%, respectively. This compares with 18.9% in 2025, while historical weighted averages over 3, 5, 10, and 15 years are 11.5%, 9.8%, 7.6%, and 7.3%, respectively.

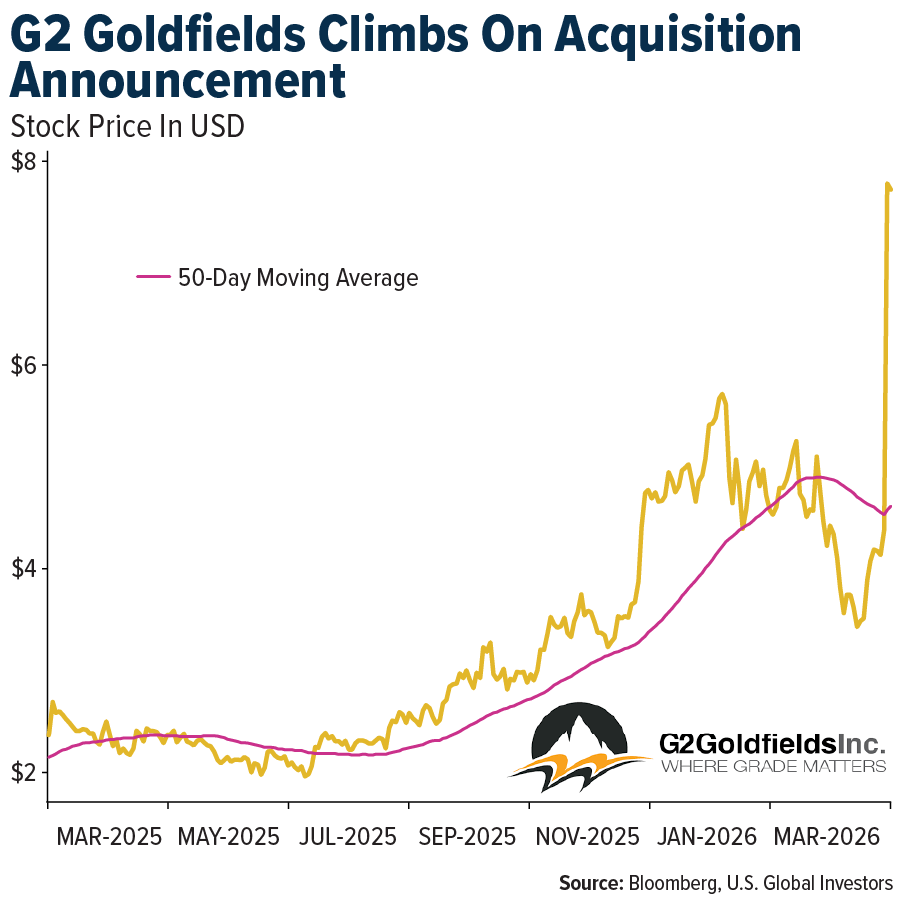

- G Mining Ventures Corp. agreed to acquire G2 Goldfields in a roughly C$3B deal that combines adjacent gold projects in Guyana. G2 shareholders will receive 0.212 GMIN shares plus a stake in a newly created explorer, G3 SpinCo, which will be funded with C$45M in cash and potential contingent value payments of up to $200M. G2 Goldfields’ share price jumped 79% on the takeover announcement.

Weaknesses

- The worst-performing precious metals for the past week were gold and palladium, still up 2.81% and 2.46%, respectively. UBS has seen a 9% reduction in ETF holdings since the onset of the Middle East conflict, driven primarily by U.S. liquidations, with global platinum outflows of 228K ounces over the same period.

- First Majestic Silver traded down almost 6% for the week when the average gold stock was up nearly 5%. First Majestic Silver reported quarterly gold and silver production that largely beat estimates; however, year-over-year gold and silver production was down 5.8% and 5.1%, respectively.

- Waning output at North America’s top gold producers is helping mining rivals in other regions catch up in the latest global rankings for annual bullion production. Newmont Corp., Agnico Eagle Mines Ltd., and Barrick Mining Corp. all reported lower gold production in 2025 compared with the prior year, and all three North American companies expect output to decline further this year. Meanwhile, global peers including China’s Zijin Mining Group Co., Africa-focused AngloGold Ashanti Plc, and Uzbekistan’s Navoi Mining & Metallurgical Co. saw production increase, according to the latest financial disclosures.

Opportunities

- The recent pullback in gold equity prices may trigger more acquisitions. Junior exploration and development stocks experienced the largest share price declines in March relative to their intermediate and senior peers, and this may act as a near-term catalyst. G Mining Ventures’ opportunistic purchase of G2 Goldfields highlights the opportunity to acquire assets after political crises that disproportionately pressure equity valuations.

- JP Morgan found that gold miners typically rally 80% over six months after gold prices bottom following market shocks. Historically, after gold fell 25% during the financial crisis, miners surged more than 50%. Gold’s 9% drop during COVID was followed by a more than 100% rally in GDX. In 2022, after gold fell 14% at the start of the Russia-Ukraine conflict, GDX rose 50%.

- Despite gold’s nearly 10% pullback from its January record amid Middle East–driven volatility, major banks remain constructive on the long-term outlook. Goldman Sachs reiterated its $5,400/oz forecast, citing continued central bank buying and expectations for 50 bps of Fed rate cuts this year. Analysts added that while near-term downside risks persist if disruptions in the Strait of Hormuz continue, a prolonged conflict could accelerate diversification away from traditional Western assets, supporting prices in the longer term, according to Bloomberg.

Threats

- U.S. federal debt surpassed $39 trillion, just 147 days after passing $38 trillion. In February, the Congressional Budget Office (CBO) released its latest economic outlook, projecting a deficit of $1.85 trillion (5.8% of GDP) for 2026, prior to the escalation of conflict involving Iran. The Trump administration has proposed increasing the US War Department’s budget by 40% to $1.5 trillion for FY27. The CBO outlook forecasts the deficit rising to $3.1 trillion over the next decade and federal debt increasing to $64 trillion.

- The Banque de France has officially ended the presence of its gold reserves in the United States, withdrawing the last 129 tons of precious metal previously held in the vaults of the Federal Reserve Bank of New York. In a report published last week, the central bank stated that the withdrawn amount represents 5% of its total sovereign gold reserves, noting that the process took place between July 2025 and January 2026, according to Bloomberg.

- Goldman Sachs recently outlined cost sensitivities to rising diesel prices across its Australian gold coverage, and now incorporates near-term cost increases into its base case, with operating costs sitting 15% above consensus in FY27. Should elevated diesel prices continue through the June quarter, they see A$20–100/oz of upside risk to FY26 AISC guidance across coverage, and a A$100–400/oz full-year impact if price pressures persist into FY27.

About the author