Strengths

- The best performing precious metal for the week was palladium, up 7.67%, followed by platinum, which rose 6.00%. The metals rallied this week on President Trump’s comments that the war could be winding down soon. Palladium was down 24% by March 26th, the worst performance among precious metals since the war began, and therefore had the most potential to move higher with the change in sentiment.

- It was a strong week for precious metals. The gains reflect that there is still positive sentiment toward owning gold, with investors waiting for some kind of resolution in the war with Iran. In general, investors stepped in to take advantage of prices that had been dragged down by the war over the past month as inflation worries rose and prospects for interest rate cuts faded, according to Bloomberg.

- Endeavour Mining delivered solid results for 2025 in Canaccord's view, with production above the midpoint of guidance and costs in line when adjusted for the increase in the gold price. The company produced 1.21 million ounces of gold in 2025, up 10% year over year, driven by a full year of production at Lafigué. Endeavour announced a record H2 2025 dividend of $200 million and reiterated 2026 production guidance of 1.09 to 1.27 million ounces. Endeavour performed in line with the GDXJ for the week.

Weaknesses

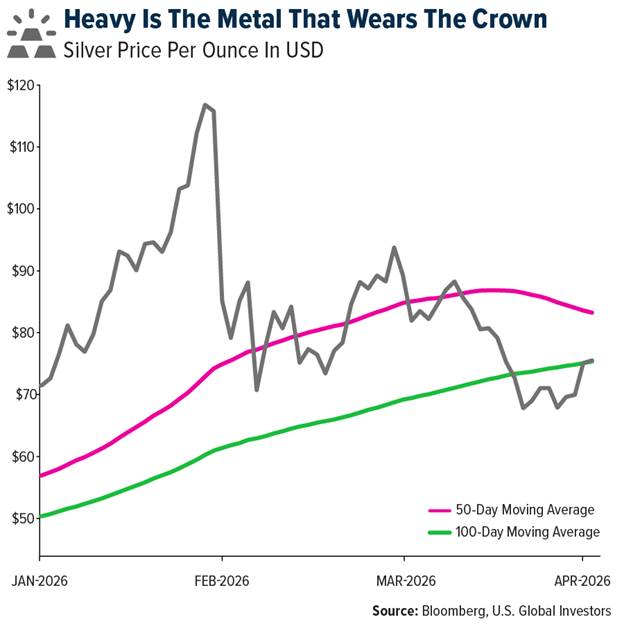

- Gold and silver were neck and neck in finishing as the worst performing precious metals for the week, though they still finished up 3.81% and 4.41%, respectively. Falling interest rates, by nearly 20 basis points for the 2-year Treasury and almost 10 basis points for the 10-year Treasury, were the key drivers of the rise in precious metal prices this week.

- Turkey sold or swapped nearly 70 tons of gold in the week to March 27, according to data published by its central bank, Bloomberg reported. The transactions come as Turkey intensifies its defense of the lira amid the ongoing war with Iran. Turkey has been one of the world’s most aggressive buyers of gold over the past decade. Since the start of the war, it has sold about 120 tons, lowering its holdings to approximately 702 tons.

- Gunmen killed more than 70 people in South Sudan over a gold mining dispute on the outskirts of the capital. The attack occurred at the Jebel Iraq mining site in Central Equatoria State, highlighting the violence linked to unregulated resource extraction. The site has been the scene of violent clashes in the past between illegal miners and mining companies, according to the Associated Press.

Opportunities

- Barrick Mining has formed an executive leadership team for its North American operations as the gold producer advances plans to pursue an initial public offering for the business. The new management team will oversee Barrick's mines in Nevada and the Dominican Republic and consists of seven positions, according to a Tuesday memo seen by Bloomberg News. Tim Cribb will serve as COO and Wessel Hamman as CFO. The spinoff, which could be worth more than $60 billion, is expected to be completed by late 2026.

- PGM miners are increasingly constructive on brownfield investments. Compared to three to six months ago, Bank of America believes the willingness to invest has increased, which is understandable given buoyant PGM prices. For now, it believes the supply response will not be excessive, but rather just enough to keep the market balanced. Platinum remains in a structural deficit, with lease rates elevated.

- Gold has not been much of a haven during the Iran war and the resulting energy shock, but its March slump may be a temporary blip, according to a Wall Street strategist. Mark Haefele, chief investment officer for UBS Global Wealth Management, stood by his bullish estimates for gold in a research note this week. UBS forecasts the precious metal will rise 35% to $6,200 an ounce by the end of June, before scaling back to $5,900 an ounce by year end, citing rising U.S. debt, de dollarization trends, and geopolitical tensions as structural drivers.

Threats

- The market is currently pricing in no change in Fed rates this year, which means gold prices face reduced tailwinds from monetary easing. UBS's forecast for gold to rise to $6,200 per ounce by June assumes a quick end to the current conflict, however, a protracted Iran conflict and continued high oil prices, which fuel inflation and push out rate cut expectations, could limit gold's near term upside. Goldman Sachs maintains a $5,400 year end target, contingent on Fed rate cuts materializing.

- Ghana sovereign risk remains a growing headwind for gold miners, as the government increasingly seeks bilateral agreements on lease extensions, royalties, and taxes, with Gold Fields facing a best case scenario of renewing its Tarkwa lease at a higher royalty rate and a worst case of losing Tarkwa entirely as Damang transitions to government ownership in April, while a new requirement that any Gold Fields mine sale must go to a local miner further constrains strategic options and depresses potential transaction valuations.

- The magnitude and duration of soaring logistics and energy costs due to rising diesel fuel will be a threat to the historically wide margins that the gold industry has enjoyed over the past year. In addition to rising diesel costs, disruptions to urea and ammonia shipments are tightening the supply of ammonium nitrate based explosives used by miners to blast ore.

About the author