NOTE: The analysis below is from the May 22nd issue of my Short Seller’s Journal. In conjunction with this, my good friend and colleague, Greg from Silver Liberties has prepared a technical analysis video of the Builders FirstSource stock chart: BLDR Technical Analysis. You can access Greg’s work at his Patreon site, to which I subscribe.

BLDR is a supplier of building materials (lumber and manufactured components) to homebuilders, sub-contractors, remodelers and consumers. Examples of its products include lumber & lumber sheet goods, wood floor and roof trusses, wall panels, windows, doors, wallboard, exterior trim etc.

My rationale for shorting BLDR is that it is a “leveraged” play on the housing market and new construction. As with homebuilders, when the market is hot BLDR’s revenues and margins soar. But when the pendulum swings back the other way, as it is now, revenues and margins dry up quickly. BLDR’s numbers have benefited both from price inflation and several “roll-up” acquisitions which exaggerated revenue growth and doubled its debt load.

BLDR’s revenues actually declined from 2018 and 2019. Then in 2020 revenues increased 17.5% YoY due to the renewed new home construction boom and commodity price inflation, both products of the Fed’s monetary policy. From 2020 to 2021, BLDR’s revenues more than doubled from acquiring BMC West. Of course, its long term debt load also nearly doubled. Revenues in Q1 2022 rose 36.1% YoY. But 58% of that gain is attributable to the BMC acquisition and to price inflation.

The Company acknowledges that demand for single-family homes drives its top-line growth. But, as we’re seeing with new home sales, home sales have started to head south. Because of this, I believe that over the course of 2022, BLDR will experience a rapid slow-down in sales growth and profitability. Compounding this problem, BLDR’s debt load increased by another 15.9% during Q1 2022. Furthermore, the Company burned $1.7 billion of cash repurchasing stock in 2021 and another $354 million on repurchases in Q1 2022 (rather than paying down debt).

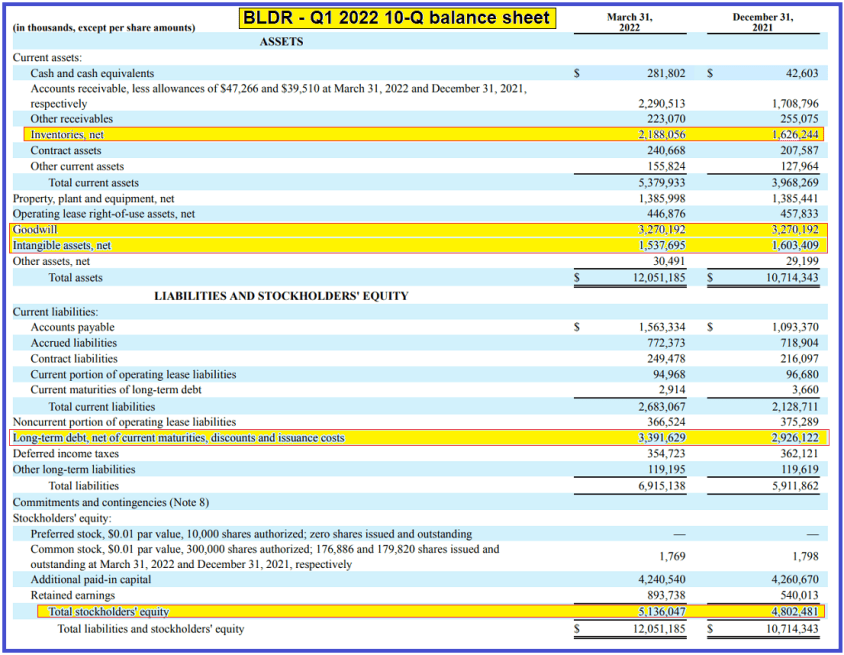

There’s also some financial red flags on its balance sheet:

First, inventories rose 34.6% in Q1 from the end of 2021. BLDR has been a big beneficiary of price inflation. Over the last couple of years it has been able to sell its inventory at prices well above the cost of building its inventory. But as new home demand declines, accompanied by falling single-family housing starts, BLDR will be exposed to considerable pricing risk. Recall the massive inventory write-downs taken by homebuilders in 2008 and 2009. That same dynamic applies to BLDR.

Another red flag is the rather plump asset value assigned to goodwill and intangible assets, which represents nearly 40% of BLDR’s assets. That $3.39 billion number assigned to goodwill is particularly troublesome. Goodwill is the amount paid for an acquisition over and above the fair value of the assets acquired. 76% of that goodwill number is a result of the BMC acquisition.

Goodwill is basically the value assigned to the various intangible “assets” of an acquisition, like brand names, customer relationships, any proprietary technology etc. That’s great when stock values are rising and the economy is robust. But goodwill can also be looked at as the amount that an acquiring company may have overpaid for the company acquired. At some point as the economics of BLDR’s business model deteriorate, that big goodwill plug will become a source of write-downs and income statement charges.

The same holds true for “intangibles.” BLDR’s intangibles are listed in the 10-K as value assigned to customer relationships, trade names, subcontractor relationships, non-compete agreements and developed technology. While goodwill is not amortized, the amortization expense of intangibles is run through the income statement. But when the housing market and economy goes bad, those “intangibles” will diminish considerably in value and will be another source of write-downs.

BLDR’s book value (stockholder equity) is $5.1 billion. But $4.8 billion of that book value is comprised of goodwill and intangible assets. As such, BLDR’s tangible book value is just $300 million. With a $3.4 billion debt load, BLDR has debt to tangible book value ratio of 10x. While this gives the Company earnings leverage in good times, when the cycle turns it will be a source of considerable financial stress.

Furthermore, BLDR does not have much room to incur inventory, goodwill and intangible write-downs (believe me, that’s coming eventually) before its book value goes negative. There will also be accounts receivable write-downs when the smaller, custom homebuilders go bust and BLDR becomes an unsecured bankruptcy court creditor.

The more I dig into BLDR’s 10-Q/K, the more I like it as a short idea. On the assumption that I’m correct about the housing market, and I believe my thesis is already starting to unfold, BLDR’s stock price will quickly deflate.

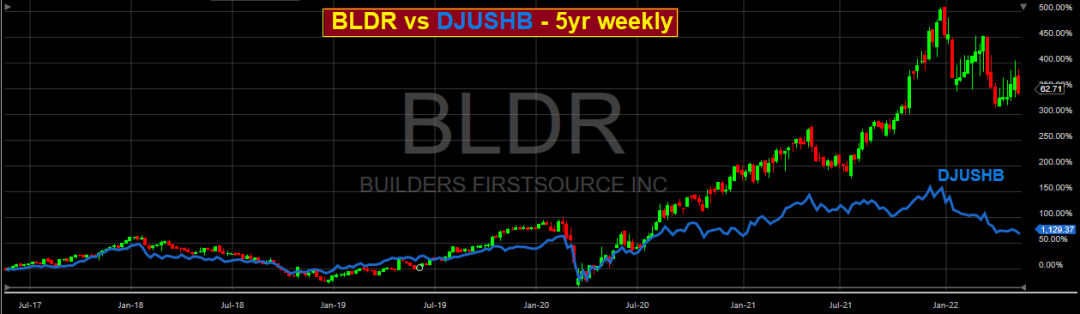

BLDR’s stock price a little more than doubled between mid-July 2021 and the end of 2021. Since then, it has already lost 29.4% of its value through Friday. In the chart above I plotted BLDR vs the Dow Jones Home Construction Index (DJUSHB) over the last five years. BLDR was tightly correlated with DJUSHB until July 2020.

I believe over the course of the rest of 2022, BLDR will, at the minimum, partially to substantially “catch down” to DJUSHB. Based on the current level of DJUSHB, this implies a price target of $30 for BLDR. But between now and the end of 2022, DJUSHB will continue to decline. I can see BLDR dropping to $20 by year-end. Keep in mind it was at $10 in March 2020.

My Short Seller’s Journal newsletter has features several ideas that have been huge home runs if not grand slams over the last 12 months, including CVNA, ARKK, HOOD, Z (Zillow), NFLS, DKNG among several others. You can learn more about SSJ here: Short Seller’s Journal information.

About the author