The investment world generally treats gold like a second-class citizen. Sure, the mainstream will sit up and take notice during a strong bull run, but generally, the financial media and investment gurus tend to spurn the yellow metal.

I'm not completely sure why the mainstream pooh-poohs gold (although I have my theories), but I do know this -- they're missing out.

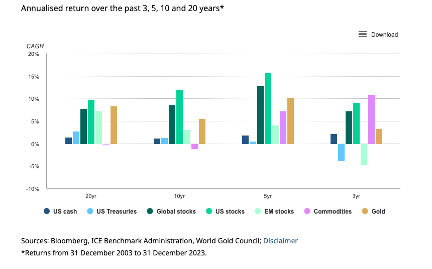

Despite the lack of love, gold has outperformed most major asset classes over the last 20 years.

As the World Gold Council notes, "Historically, gold has generated long-term positive returns in both good and bad economic times."

Taking a longer view, the returns on the yellow metal have been similar to equities, and gold has outperformed bonds since 1971.

On average, the price of gold has increased by nearly 8 percent annually since '71 when Nixon severed the dollar's last tie to gold.

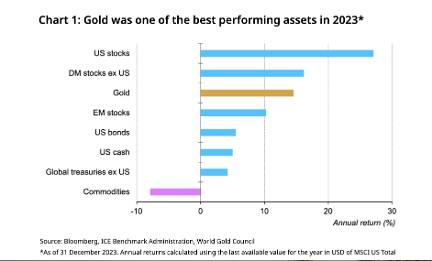

The price of gold was up about 13 percent in 2023 and was among the best-performing assets. Gold outperformed emerging market stocks, U.S. bonds, the U.S. dollar, global treasuries, and commodities in general. The only asset classes that performed better than gold were U.S. stocks and developed-market foreign stocks.

Gold also tends to be less volatile than other asset classes.

This is due to its diverse sources of demand. As the World Gold Council put it, this diversity "gives gold a particular resilience and the potential to deliver solid returns in various market conditions."

"Gold is, on the one hand, often used as an investment to protect and enhance wealth over the long term, but on the other hand, it is also a consumer good, via jewelry and technology demand. During periods of economic uncertainty, it is the counter-cyclical investment demand that drives the gold price up. During periods of economic expansion, the pro-cyclical consumer demand supports its performance. Combined, these factors give gold the ability to provide stability under a range of economic environments."

Gold serves particularly well as an inflation hedge. Since 1971 it has outpaced both U.S. and and global CPI. The yellow metal also tends to do well in high inflation periods. This has proved true during the recent inflationary cycle.

The price of gold has increased by about 29 percent since June 2021 (as inflation started heating up). In that same period, CPI increased by 12.30 percent based on official Bureau of Labor Statistics data.

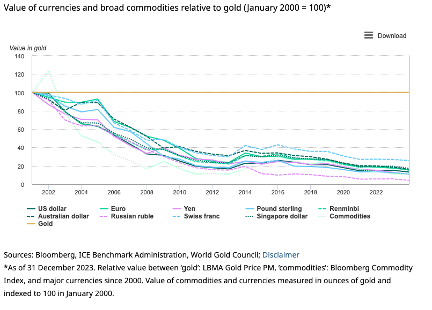

Ultimately, gold is money. And it is sound money. Every major currency has depreciated significantly compared to gold.

Despite its strong performance over time, most investors don't hold any gold in their portfolios. Is it perhaps time to change that?

The investment world generally treats gold like a second-class citizen. Sure, the mainstream will sit up and take notice during a strong bull run, but generally, the financial media and investment gurus tend to spurn the yellow metal.

I'm not completely sure why the mainstream pooh-poohs gold (although I have my theories), but I do know this -- they're missing out.

Despite the lack of love, gold has outperformed most major asset classes over the last 20 years.

As the World Gold Council notes, "Historically, gold has generated long-term positive returns in both good and bad economic times."

Taking a longer view, the returns on the yellow metal have been similar to equities, and gold has outperformed bonds since 1971.

On average, the price of gold has increased by nearly 8 percent annually since '71 when Nixon severed the dollar's last tie to gold.

The price of gold was up about 13 percent in 2023 and was among the best-performing assets. Gold outperformed emerging market stocks, U.S. bonds, the U.S. dollar, global treasuries, and commodities in general. The only asset classes that performed better than gold were U.S. stocks and developed-market foreign stocks.

Gold also tends to be less volatile than other asset classes.

This is due to its diverse sources of demand. As the World Gold Council put it, this diversity "gives gold a particular resilience and the potential to deliver solid returns in various market conditions."

"Gold is, on the one hand, often used as an investment to protect and enhance wealth over the long term, but on the other hand, it is also a consumer good, via jewelry and technology demand. During periods of economic uncertainty, it is the counter-cyclical investment demand that drives the gold price up. During periods of economic expansion, the pro-cyclical consumer demand supports its performance. Combined, these factors give gold the ability to provide stability under a range of economic environments."

Gold serves particularly well as an inflation hedge. Since 1971 it has outpaced both U.S. and and global CPI. The yellow metal also tends to do well in high inflation periods. This has proved true during the recent inflationary cycle.

The price of gold has increased by about 29 percent since June 2021 (as inflation started heating up). In that same period, CPI increased by 12.30 percent based on official Bureau of Labor Statistics data.

Ultimately, gold is money. And it is sound money. Every major currency has depreciated significantly compared to gold.

Despite its strong performance over time, most investors don't hold any gold in their portfolios. Is it perhaps time to change that?

About the author