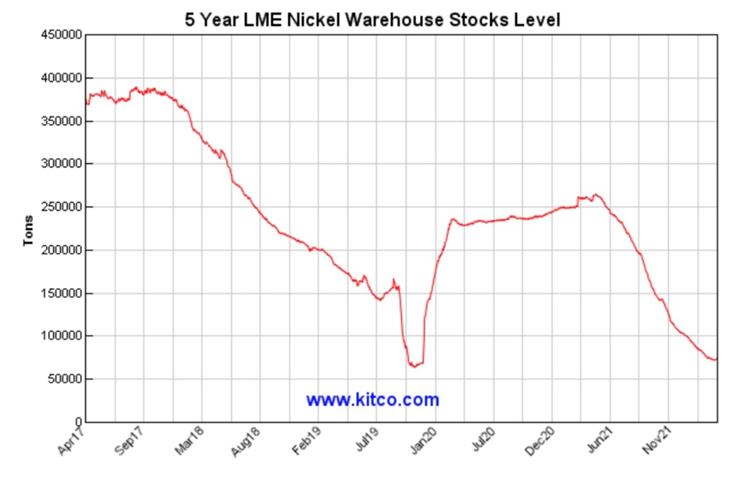

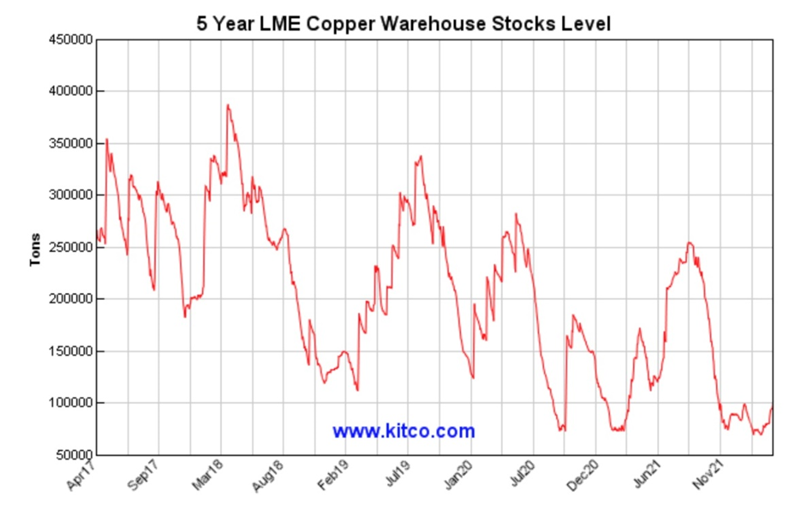

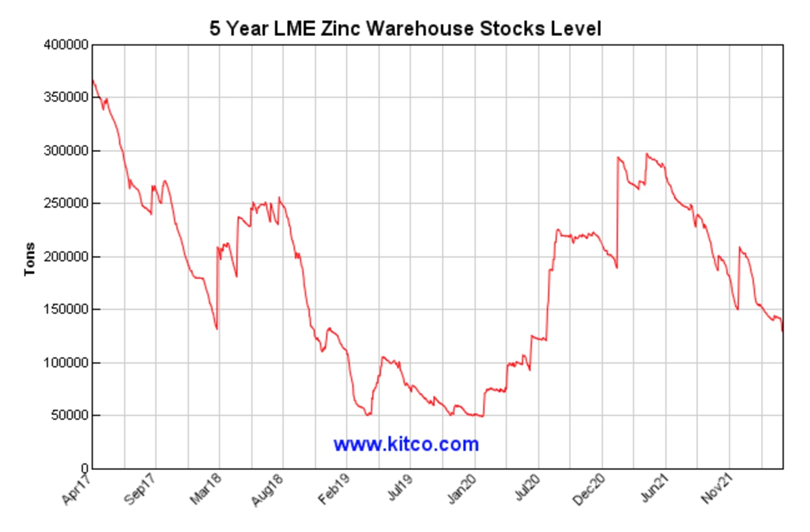

Bloomberg reported on Thursday that inventories across London Metal Exchange warehouses have “dropped to perilously low levels, raising the threat of further spikes in everything from aluminum to zinc.”

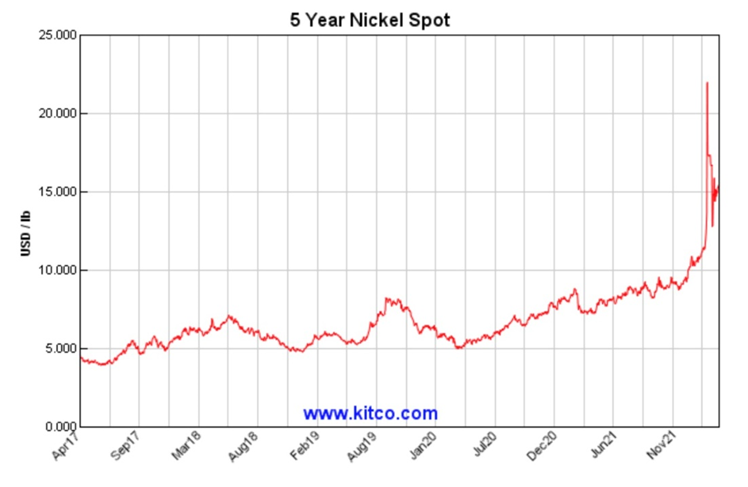

Nickel remains at risk of further turmoil, with the “big short” that sparked the crisis on the LME still mostly in place. Volumes have all but dried up and prices are stuck at historically high levels.

“There’s still a lot of nervousness and cautiousness in the market,” the head of commodities strategy at BOCI Global Commodities, said in a media report, Friday. “Nickel is likely to remain highly volatile and due to geopolitical uncertainty and low liquidity, we won’t see a return to normal any time soon.”

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Available stockpiles across the six contracts on the LME are at their lowest levels since 1997. Goldman Sachs warned that copper is “sleepwalking towards a stockout” and zinc inventories fell more than 60% in under three weeks, as Trafigura Group purchased large volumes. The sharp drop echoes a similar drawdown in copper last year, when stocks of the red metal plunged to the lowest since 1974.

After briefly spiking above $5 a pound a month ago, on historically low inventories, copper prices have slipped back.

However in its report, Goldman points to “an extreme fundamental turn” for copper, whose stocks on metal exchanges for the first time in a decade declined through March instead of rising.

Analysts at Goldman were quoted saying the bank believes “higher prices are an inevitability,” needed to stimulate more scrap copper supply and to accelerate demand destruction to balance the market. The analysts reportedly doubled the deficit of refined metal expected for this year from previous estimates to 374,000 tonnes and also increased substantially the shortfalls projected over the next two years.

Goldman upped its three, six and 12-month price targets, and forecasts copper climbing to 13,000 a tonne within a year’s time. The analysts see a new all-time high for the copper price by mid-year.

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Source: Kitco

Besides copper, nickel and zinc, the markets for other electrification and decarbonization metals look equally bullish.

The price of lithium is up more than 400% year on year, as automakers race to secure supplies, expecting a surge in demand for the EV battery ingredient.

Tesla’s Elon Musk had this to say about the lightweight metal, tweeting:

Price of lithium has gone to insane levels! Tesla might actually have to get into the mining & refining directly at scale, unless costs improve.

From December 2020 to December 2021, graphite prices rose 20% to roughly $680 a tonne, according to Benchmark Mineral Intelligence data, after spending most of 2020 below $700/t. It is estimated that the natural flake graphite market could reach a deficit as soon as 2023, with few new sources being developed around the world.

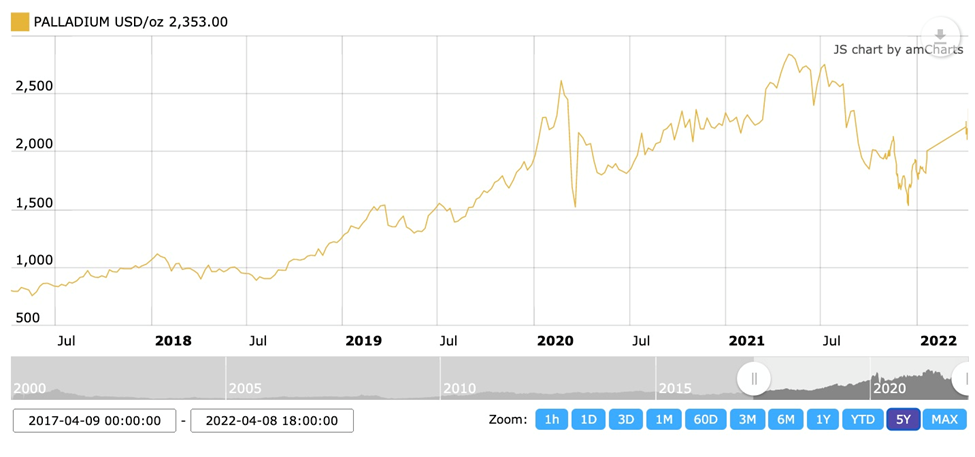

A string of annual supply deficits starting in 2018, combined with higher sales of gasoline vs diesel units, culminated in palladium’s historic price pinnacle of $2,830 per ounce in May, 2021.

Source: Kitco

Source: Kitco

The platinum-group metal has enjoyed a spectacular ride since Russia invaded Ukraine at the end of February. Year to date, spot palladium has climbed an impressive 33%.

The auto sector, where palladium is heavily used in gasoline-powered catalystic converters, is facing a significant supply crunch with two Russian refiners recently barred from Western markets.

The London Platinum and Palladium Market, (LPPM) announced on Friday that it has suspended immediately the Gulidov Krasnoyarsk Non-Ferrous Metals Plant “Krastsvetmet” and the Prioksky Plant of Non-Ferrous Metals “PZCM” from its Good Deliveries Lists.

While these aren’t the first refiners to be suspended due to sanctions resulting from the Russian attack on Ukraine — a month ago the London Bullion Market Association dropped all six Russian gold and silver refineries from its Good Deliveries List — the latest move is expected to have a greater impact on the PGE markets than gold and silver. That’s because, while most of the gold and silver Russia produces stays within the country, the country produces up to 30% of the world’s palladium supply and 10% of worldwide platinum.

“Our immediate and conservative estimate of the scale of this disruption suggests that more than 102 tonnes of PGM output will be disrupted as a result of this decision, considering the epic scale of these refiners,” commodity analysts at TD Securities were quoted by Kitco News.

June palladium futures last traded at $2,420.10 an ounce, up 8.86% on the day.

The outlook for silver, used extensively in solar panels, among a wide range of industrial applications, is especially promising this year. After rocketing to $28 an ounce in August of 2020, silver has held its own within a relatively narrow range of between $22 and $25.

Source: Kitco

Source: Kitco

According to the Silver Institute, global demand for silver is expected to hit a record 1.112 billion ounces in 2022, driven by industrial fabrication, which is forecast to improve by 5%, “as silver’s use expands in both traditional and critical green technologies.”

After shifting to a deficit in 2021 for the first time in six years, SI says the silver market is expected to record a supply shortfall of 20 million ounces this year.

The cross-the-board metals shortage hearkens back to last year. Inventories started dropping as industrial activity roared back on post-pandemic economic recovery in some of the world’s largest economies. According to Bloomberg, Metals like aluminum and zinc came under pressure in Europe as surging power prices made some plants unprofitable, leading to closures. More recently, supplies from Russia’s giant metal producers have become less desirable and harder to ship following the country’s invasion of Ukraine.

Many analysts see metals heading higher as shortages on the LME and the wider physical markets deepen.

Another respected investment bank, JPMorgan, says commodities could surge by as much as 40%, explaining that while allocations appear to be above historical averages, they are not overweight, suggesting further upside and investor gains.

Conclusion

Of course, mined commodities are not only rising to due to shortages; supply chain disruptions owing to covid-19 and strong demand as economies bounce back from the pandemic are also major factors.

According to Wired, ‘The Supply Chain Crisis Is About to Get a Lot Worse’. While previously a supply chain was 80% predictable and 20% surprises, now the numbers are reversed. The new reality “has backlogs and breakdowns as the new normal,” states the article, quoting a professor of supply chain strategy of Cranfield University in the UK who says, “We used to occasionally have black swan events. The problem at the moment is we have a whole flock of black swans coming at us.”

The disruptions boost costs across each individual supply chain that have to be recovered, usually by passing them onto consumers, thus fueling the inflationary cycle. Inflation in the United States, Canada and the UK this year reached multi-decade highs.

Pent-up and new demand for infrastructure and manufactured goods is also expected to boost the prices of industrial metals.

While the United States in November passed a trillion-dollar infrastructure package that includes, among other things, money for roads, bridges, power & water systems, transit, rail, electric vehicles, and upgrades to broadband, airports, ports and waterways, China is looking to outspend it by a large margin.

At Beijing’s behest, local governments have reportedly drawn up lists of thousands of “major projects,” which they’re being put under intense pressure to see through. Planned investment this year amounts to at least 14.8 trillion yuan ($2.3 trillion), according to a Bloomberg analysis. That’s more than double the new spending in the infrastructure package the U.S. Congress approved last year, which totals $1.1 trillion spread over five years.

Notably, the composition of the stimulus spending will be less on infrastructure than manufacturing, including factories, industrial parks and technology incubators. The construction push is part of the central government’s plan to meet its targeted 5.5% growth rate this year.

In Beijing alone, the list of major projects requiring 280 billion yuan (a billion yuan = USD$157B) in investment this year includes a panda breeding center, a Legoland theme park, and an electric vehicle factory operated by tech company Xiami Corp, Bloomberg writes.

The new “commodities supercycle” touted by many including Goldman Sachs, may be tied to the infrastructure deficits many countries need to try and reduce, along with the global threat of climate change, the evidence for which is growing stronger each year, and is driving economies to rapidly shift away from carbon-emitting energy sources to low-carbon or carbon-free alternatives.

China, however, cannot be counted out as requiring metals both for traditional “blacktop” infrastructure and green projects needing a broad range of electrification/ decarbonization metals. Unless new deposits are developed to address the widening shortages for raw materials, amid continuing supply chain issues, we should expect high metal prices to continue for the foreseeable future.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.