In our 2022 macrocast, it was stated that the only thing predictable about the year ahead would be its unpredictable nature and wild volatility. Well, at least we got that right.

So, one year ends and a new year begins. The year 2022 unfolded in a manner similar to years past when The Fed was allowed to pretend and promote the idea of responsibility, prudence and balance sheet reduction. You might have thought that, collectively, the markets would have learned by now to see through this nonsense and, in a way, it appears they have.

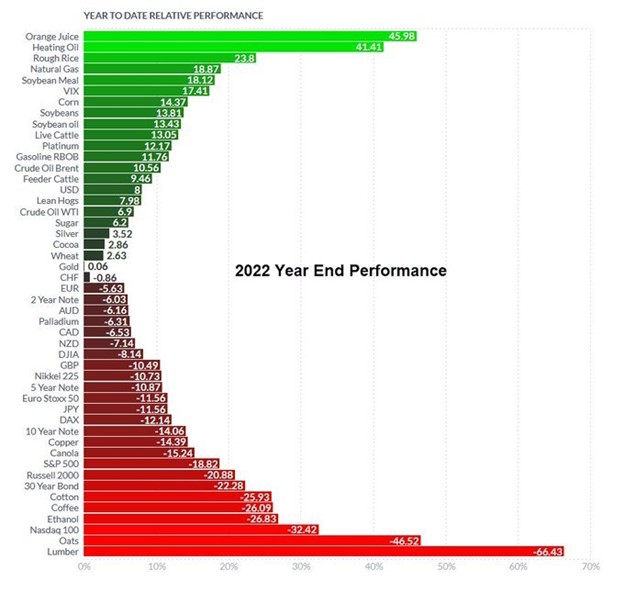

If, in January of 2022, I had written that the dollar index was set to spike 25% and that nominal rates were going to double, triple or quadruple depending upon duration, I'm pretty sure that it would have come with a forecast of sharply lower precious metal prices. Instead, at the close of 2022, Comex gold prices were down just $2.50. Yes, you read that right. On the year, gold was down $2.50 or about 0.13%. Comex silver fared even better with a gain of 63¢ and a closing price of $24.01. That's up 2.7% on the year.

Holders of other commodities and asset classes didn't fare as well, as you can see below:

The late 2022 rally that drove gold and silver back into the green on the year is very likely the result of a "market" that did finally learn to see through The Fed's blather and bluster. As 2023 begins, we're set to witness another easing cycle and, eventually, QE program. Gold and silver can see this coming and have reacted in preparation. Other markets will soon do the same.

But this next cycle of Fed easing is not yet upon us and, therefore, the first three to six months of the new year may continue to frustrate all of us as we await the eventual breakout to the upside.

For 2022, I had expected The Fed to reverse course by mid-year and begin cutting rates by late year if the S&P fell by 20% and the yield on the 10-year note surpassed 3.25%. Well, the S&P did, in fact, fall 20% and the yield on the 10-year note reached 4.45% and yet, still no cuts. So what's the deal?

What The Fed failed to predict was the Russian invasion of Ukraine on February 24. This new war added a whole new dynamic to the economic uncertainty that prevailed as 2022 began. As such, while The Fed may have intended to act more quickly to stem inflation by raising rates, they were forced to delay. This gave time for inflation to gain even more momentum and reach levels not seen in over forty years.

As The Fed persisted in their QE and waited too long to begin raising rates in 2022, they will be similarly persisting with rate hikes and waiting too long to restart QE in 2023. This will ultimately lead to a much sharper economic contraction than is currently expected and, once the Fed starts cutting again, it will then lead to much lower rates than currently forecast, too.

Think of it like a pendulum. However, instead of the swings becoming more narrow over time, in this case the swings become more wide. The paradigm-changing event was the initial QE program of March 2009. Since then, each subsequent rate cut and QE program has gotten larger and the inflationary impacts have gotten more substantial.

- QE 1: $600B in March 2009

- QE 2: $650B in November 2010

- QE 3: $1.1T in October 2012

- QE 4: $4.5T in March 2020

- QE 5: TBD beginning sometime late 2023 or early 2024.

In the simplest terms, how and why can we be so certain that the next QE program will be the largest yet? It's just the math.

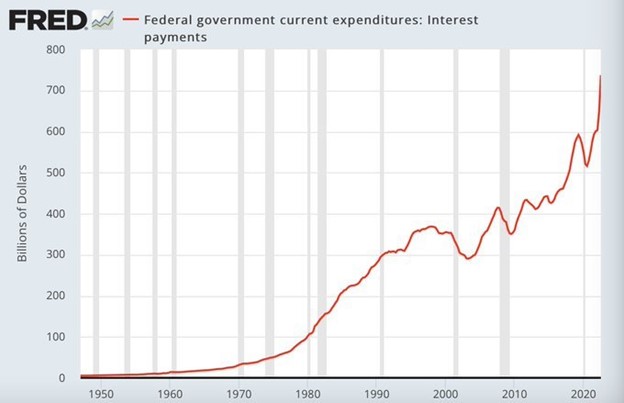

As rates rose in 2022, the budget line item of "interest on the national debt" ballooned to nearly $750B/year. If rates were to continue higher, this one expense would soon eclipse other "necessary" government outlays like social spending and defense. This cannot, and will not, be allowed.

At present, rates have continued higher for the basic economic reason of bonds having more sellers than buyers. This leads to lower bond prices and higher rates. Traditional buyers have left the building. The ECB? Not buying treasuries. Neither is the PBOC nor the BoE. And you can forget about the BoJ coming back anytime soon as they're desperate to manage their own bond market.

So The Fed eventually becomes the buyer of last resort at U.S. Treasury auctions, otherwise rates spike, the U.S. economy contracts dramatically, tax receipts plummet and the entire Ponzi-style debt scheme implodes. Wanting to forestall this collapse as long as possible is why QE has persisted as the dominant Fed policy since 2009 and it's why The Fed will be forced to get back in the game much sooner than most 8-figure Wall Street economists expect.

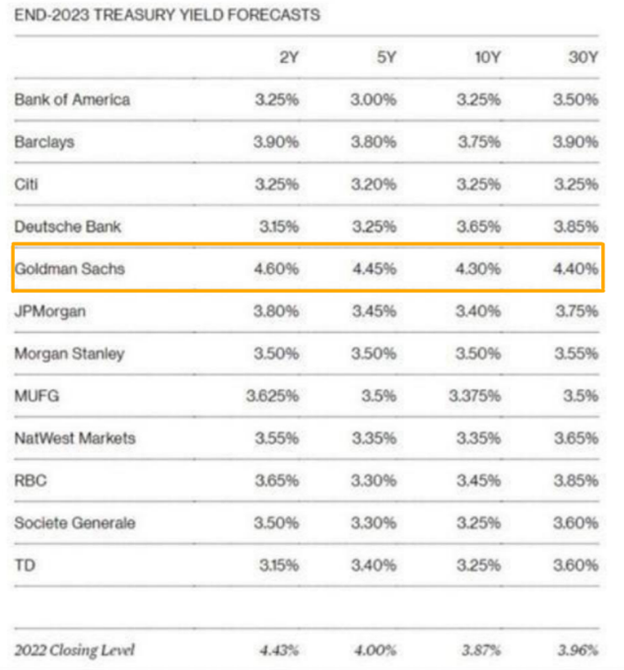

Speaking of those Wall Street guys, we enter 2023 with many of them still employed after another year of dreadful forecasting and many of them making the same mistakes as 2019, which is the most recent year that's analogous to the year ahead. As 2019 began, nearly every economist and sell-side analyst was forecasting higher rates in the months to come. The ignominious Jan Hatzius of Goldman Sachs was projecting the yield on the benchmark U.S. 10-year note to rise from 2.50% to 4.5-5.0% by year end. Instead, rates fell and finished the year at 1.50%. You'd think he'd have learned his lesson but here's ole Jan making the same mistake in late 2022.

We called them on it back then and forecast that 2019 would resemble 2010, instead, and we were right...even though no one has yet to offer me an 8-figure salary. And now here's the deal. The year ahead is going to play out like 2019, and 2010 before it, as the markets begin to realize once again that The Fed is trapped with no way out but to cut rates and restart QE.

Maybe a better title for this post would have been "2010 +9 +4" but, since the world in 2023 is collectively marching lockstep into very dangerous territory, "One Step Beyond" seemed more appropriate. Much of the chaos that drove 2022 will begin to spin out of control in 2023 but The Fed, and their media minions, will have you believe that they are all-knowing demigods who can successfully manage every possible economic and geopolitical outcome. Nothing could be further from the truth. From their ivory towers, your economic masters can only guess, hope and pontificate, all while that economic pendulum swings ever more widely.

The key though, will be patience...which was another possible title for this year's macrocast. Just as my 2022 expectation of a Fed reversal and pivot was delayed by some of the year's unforeseen events, my expectation may continue to be delayed a little in 2023. The most important factor pushing The Fed will be the economic data and just how quickly the U.S sinks into a recognizable and undeniable recession.

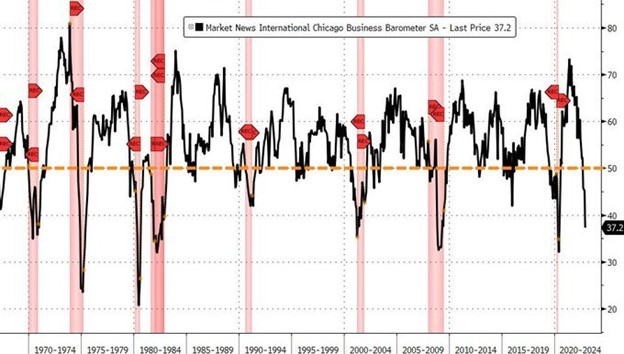

Already, the manufacturing and service sector PMIs are deeply into economic contraction territory and these measures have a perfect track record of predicting the past eight recessions.

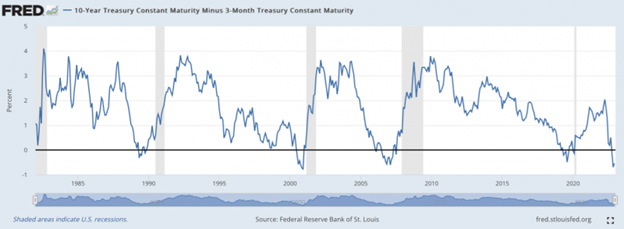

And speaking of recession predictors, have you seen the current yield curve inversion. Short-term interest rates that are higher than long-term interest rates is another signal that usually precedes recessions.

So what does all of this portend for precious metal prices in 2023? Well, they're going higher, that's for certain. However, before we get to that forecast, there are a few other mitigating factors we need to discuss.

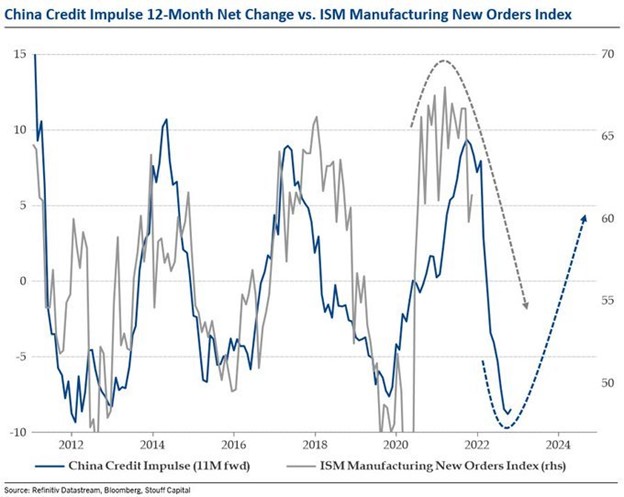

First of all, what about that "Chinese Credit Impulse" that we discussed in last year's macrocast? It was expected that a reopening of the Chinese economy would increase demand for all commodities, including gold and silver. Instead, China continued their foolish "Zero Covid" policy all year and only began to ease up in late December. So, can we expect that pent up commodity demand to be unleashed in 2023? Maybe. You'd better keep an eye on this, especially later in the year by the looks of this next chart.

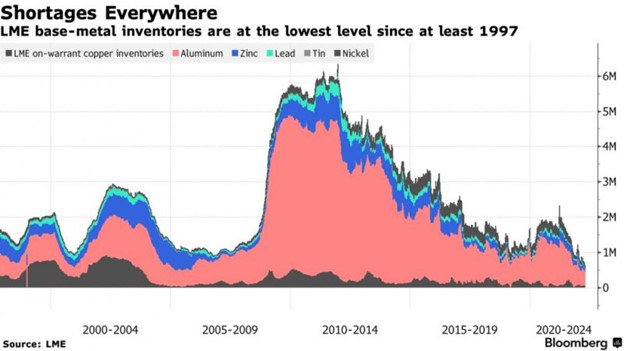

And if Chinese commodity demand reemerges in 2023, how will that impact the supply of all physical metals? As you can see below, base/industrial metal stockpiles have been steadily declining over the past decade.

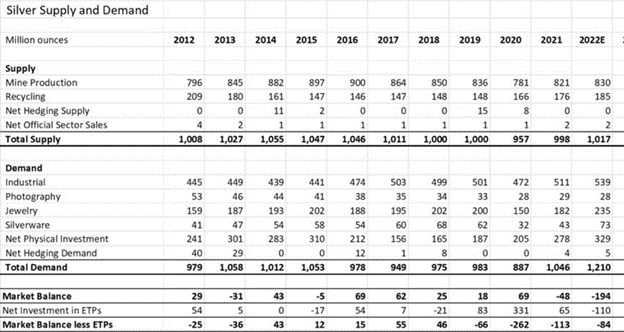

On top of this, don't forget that The Silver Institute came out in November with a forecast of a global supply deficit of 194,000,000 ounces: https://www.silverinstitute.org/global-silver-demand-rising-new-high-2022/

On the chart above, how does the "industrial demand" picture change if China comes back as a major hoarder of silver? As mentioned, this forecast was made in November, or about two months before China finally began to reopen its economy.

So, let's begin to sum up. Let's start with what we know...or what we think we know...about the year ahead.

- the US and global economy is going to fall into a sharp contraction and undeniable recession

- the backward-looking global central banks will be late to react, as usual

- by June at the latest, The Fed will begin discussions of future rate cuts

- by December at the latest, The Fed will begin discussions of a new QE program

- the economic and monetary situation will mirror 2010 and 2019

- as such, gains in the Comex precious metals will mirror 2010 and 2019, too

With all of the above in mind, perhaps we should begin our 2023 price forecast with a look at the charts from 2010 and 2019. Again, these were years that began under very similar economic and monetary circumstances. Namely, the belief was widely held that rates were headed higher in the months to come, that all QE programs had ended and that The Fed would soon "normalize" its balance sheet.

The most important lesson from the charts above is this: Look at the price action for the first half of each year. It's mostly sideways!

Though The Fed had preached responsibility in 2010, a contracting economy led them to announce QE2 in November of that year. The Comex gold price began to sniff this out three months in advance and then rallied 22% into year end.

And though all of Wall Street was expecting higher rates and Fed prudence in 2019, a contracting economy led The Fed to hint at rate cuts by March of that year and then they actually began cutting rates in June. Comex gold responded by moving up 24% in three months.

The lesson? If you had bought the lies of The Fed, their sycophant media and fully-captured Banks, you'd have been ill-prepared for the rallies to come. Additionally, if you had grown weary and impatient while the metals began the year trading sideways, you'd have missed out on some tremendous, short-term price moves.

So again and just as in 2010 and 2019, the single most important thing you can do is think for yourself, prepare for what you know is coming, and then be patient as you wait for it to unfold.

As such, what should you expect in terms of price? Let's just use 2010 and 2019 as a guide.

Knowing what you know, why wouldn't you expect some sideways price action through Q1 and into Q2? That's what I expect. But then the fun starts. At some point, The Fed will begin to admit that their delayed inflation response and inaction has led to an overreaction that has driven the U.S. economy into the ditch. Will we get hints of this as soon as the March 21-22 FOMC? How about the FOMC meeting scheduled for June 13-14? Can/will they hold off until then?

But truth be told, the timing of the eventual "Pause & Pivot" doesn't matter as long as you understand that the policy shift is an eventuality and, as such, you simply remain patient in waiting for it to be announced.

For Comex Digital Gold, this means that price likely remains rangebound a little while longer. Price has consolidated its 2020 breakout to all-time highs by process of a massive "bull flag" on the chart. Spring of 2022 saw a false upside breakout of this flag and autumn of 2022 saw the reverse, a false downside breakout. As 2023 begins, you can see that price is squarely back into the confines of the flag and its likely to remain there through the first third or half of the year.

But as we look ahead and project price deeper into 2023, we must consider two things that history has taught us:

- As stated above, price quickly rallied more than 20% once economic and monetary reality was realized back in 2010 and 2019. The midpoint of the current flag/consolidation pattern is $1900. If we add 20% to that, we get $2280.

- Gold, silver...really almost anything...when making a new all-time high, will pick up a speculative surge of fresh cash and rally another 10% before pulling back and consolidating its gains. The current all-time high for Comex Digital Gold is near $2100. If we add 10% to price for the coming, new all-time high, we get $2310.

So, OK, that's sounds about right. Expect Comex gold to trade to $2300 sometime before 2023 draws to close.

What about Comex Digital Silver? Well, that's a little more complicated for the reasons listed above and, as you know, Comex silver is subject to 2-3X the volatility seen in Comex gold when prices are rallying. So, if Comex gold is expected to rally over 20% intrayear, why can't Comex silver be expected to rally 40% or more?

Comex silver displays its own bull flag/consolidation on its long-term charts. It flirted with a breakout in March of 2022 and then showed a false breakdown later in the year. However, it's back to near the middle of its range and wanting to move higher as 2023 begins.

And you might be asking yourself, how did Comex silver fare in 2010 and 2019? As you can see below, it rallied nearly 70% in the back half of 2010 and about 36% from late May to early September 2019.

So why not split the difference? Let's say that Comex silver hangs around the middle of this current range for the first 4-6 months of 2023 but then, as The Fed edges closer to making that inevitable shift to rate cuts and QE, it breaks out, catches another massive speculator bid and moves up 50% to about $38 sometime before year end.

Now maybe most of this sounds crazy but all I've really done here is lay out for you what has happened in the recent past and is therefore quite likely to happen again. You can write it off and stick with the mainstream narrative or you can think for yourself and consider the old adage of history not necessarily repeating but rhyming.

Oh, and one more thing, if we're right about all of this....how The Fed will soon shift policy, just as they did in 2010 and 2019...then you should probably take a few moments to remind yourself of how the Comex precious metals fared in 2011 and 2020. This first year of the easing cycle typically just whets the appetite for what's to follow.

Of course, there are other factors that will come into play over the months ahead. Who can predict how NATO vs. Russia will play out and what will happen in the battle of the U.S. vs. China over Taiwan? What about Lil Kim in North Korea? And how will the increasing speed of de-dollarization by the BRICS+ impact things? The answers to these questions are all unknowable as 2023 begins and geopolitics must always be monitored if you're going to follow the precious metals. Keep your guard up and hope for the best, however, preparation and diligence are your best tools for managing the year ahead.

To that end, I strongly urge you to consider joining the global community of TFMR. Precious metals are our daily focus but, for the bigger picture, the membership community adds valuable content each and every day. A subscription to TFMR is perhaps the best investment for your financial and mental well-being in 2023 and it's only $15/month. Join us and we'll get through all of this together.

Thanks for taking the time to read this year's macrocast. I hope to see you at TFMR soon.

About the author

Our Ask The Expert interviewer Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.