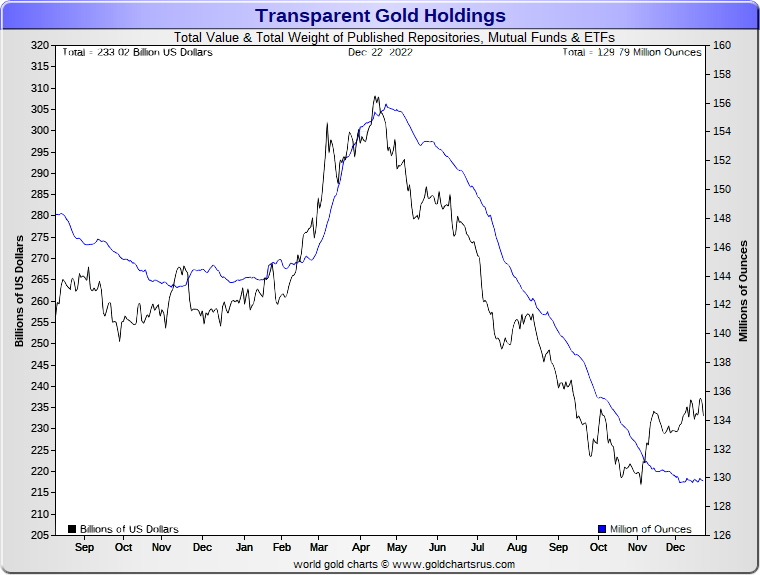

Late-year gold ETF stockpile gains hint at renewed institutional interest

In 2022 gold held its own while the rest of the investment universe was taken to the woodshed. So what will 2023 bring? Is gold setting the stage for a return to all-time highs at $2075 per ounce? Many prominent analysts think that might be the case, particularly in light of the strong finish to 2022. If gold does return to all-time highs in 2023, fund and institutional interest will likely be a key catalyst. Over much of 2022, that sector has been a net seller of gold, as reflected in the 17% reduction in stored gold stockpiles between May and November, according to tracking by GoldChartsRUs. However, the last two months of the year hint that a shift might be underway.

“There are no simple answers for the investment community,” says Australia’s sovereign wealth fund, which recently announced making its first gold purchases ever. “Traditional approaches have delivered strongly, but it is doubtful they are fit for the purpose in the future.… In this kind of environment, there is a real risk of simultaneous slow growth, high unemployment, and rising prices that has some parallels with the stagflationary period that struck developed markets in the 1970s.” The fund, according to a Reuters report, questions the effectiveness of the traditional 60/40 portfolio arguing that an “investment shift” is necessary to counteract “a time of war, inflation and climate change.”

Editor’s note: Gold ETFs are the preferred ownership vehicle among funds and institutions. Over the years, there has been a tight correlation between stockpile growth and a rising gold price.

Chart courtesy of GoldChartsRUs.Com

Chart courtesy of GoldChartsRUs.Com

Short & Sweet

CONTRIBUTING TO SAXO BANK’S ANNUAL DIGEST OF OUTRAGEOUS PREDICTIONS, commodity analyst Ole Hansen says that 2023 will be the year “that the market finally discovers that inflation is set to remain ablaze for the foreseeable future.” He foresees a confluence of influences on the “hardest of currencies” – a global war economy mentality, massive energy transitions, and rising global liquidity as central banks move to belay “a debacle in debt markets.” As a result, he predicts, “gold slices through the double top near USD 2,075 as if it wasn’t there and hurtles to at least USD 3,000 next year.”

“SOARING INFLATION,” REPORTS FINANCIAL TIMES, “IS BEING MET by rising interest rates, the slowing of central bank asset purchases and fiscal shocks, all of which are sucking liquidity, the ability to transact without dramatically moving prices, out of markets. Violent, sudden price moves in one market can provoke a vicious loop of margin calls and forced sales of other assets, with unpredictable results.” The governing theme in high-level discussions about the financial markets is “liquidity.” In fact, it’s all about liquidity, or more precisely put – the lack of it. We do not recall a time when the warnings of a possible financial meltdown were more prolific and urgent.

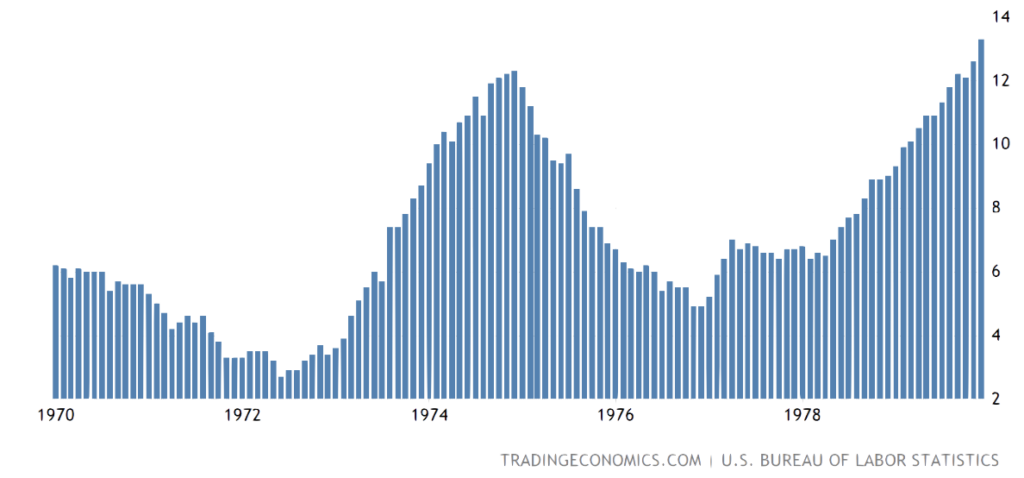

DURING THE 1970s, BIG SWINGS UP OR DOWN in the inflation rate were commonplace, but there was no mistaking the overall trend. Stagflation, the real culprit back then and the one feared most now, began slowly, gathered pace, became very sticky, and stayed so through the early 1980s. “Once sticky prices are rising,” writes John Authers in his Bloomberg column,” it’s a sign that inflation psychology is becoming embedded. And sticky price inflation is still very high. On a year-over-year basis it’s at a four-decade high, while inflation over the last three months is running a bit less than at the peak earlier this year — but still at a pace unseen in decades. Once sticky prices come unstuck, will they keep trundling upwards? It’s a crucial question, to which we don’t yet have the answer:”

Editor’s note: Given the fact that the financial press was caught completely off-guard when inflation rocketed higher last year, one wonders if it is being hasty by declaring it has already peaked. Goldman Sachs is calling for a 43% gain in commodity prices next year – much of it centered around energy and industrial metals. If the reality is anywhere near the prediction, it is likely to drive retail inflation much higher. Only the timing is in question. Peak anything in an inflationary environment is a pipe dream – including inflation itself. We should keep in mind that the current inflation is the product of the largest money-printing binge in history, and most, if not all, the global central banks participated. You can’t just wish that away.

US inflation rate 1970-1979

(%, monthly, annualized)

Chart courtesy of TradingEconomics.com

THE MOST OPTIMISTIC GOLD PRICE PREDICTION we have seen in the year-end forecasting sweepstakes comes from Swiss Asia Capital’s Juerg Kiener. He thinks the metal could reach $2500 to $4000 per ounce in 2023. “It’s not going to be just 10% or 20%,” he told CNBC Street Signs, but a move that will “really make new highs.” In that same article, Nikhil Kamath, co-founder of India’s largest brokerage, recommended investors allocate 10% to 20% of their portfolios to gold.

“IN MARKET PARLANCE, A REAL INTEREST RATE is one that is above inflation,’ writes Jeffrey Bartash in a MarketWatch report. “The rate of inflation right now, using the Fed’s preferred personal-consumption-expenditures, or PCE, price gauge, is 6%. That’s markedly higher than the current 4.25% to 4.5% fed-funds rate” If you are a regular reader of this newsletter, this argument will sound familiar. We are a very long way from achieving the positive real rate milestone. Too, the PCE price index, though preferred by the Fed, excludes food and energy prices, so how realistic is it as an accurate measure of inflation? The inflation rate, as measured by the more worldly Consumer Price Index, is 7.1%. Shadow Government Statistics, which tracks the inflation rate using the Labor Department methodology of the 1980s, puts the inflation rate at 15%. By either measure, the ten-year Treasury yield at roughly 3.5% leaves a substantial gap that needs to be breached for investors to achieve a real rate of return.

THE WORLD GOLD COUNCIL RELEASED ITS OUTLOOK FOR 2023 IN DECEMBER, saying that the “interplay between inflation and central-bank intervention” will be a key determinant in gold’s performance. It sees challenges ahead for global central banks “as the prospect of slower growth collides with elevated, albeit declining inflation” gold, it says, “could provide protection as it typically fares well during recessions, delivering positive returns in five out of the last seven recessions (See chart below). But a recession is not a prerequisite for gold to perform. A sharp retrenchment in growth is sufficient for gold to do well, particularly if inflation is also high or rising.” WGC goes on to say that the economy might not follow a “well-telegraphed path” in 2023 warning that “hypervigilant central banks” might overtighten resulting in “more severe economic fallout and stagflationary conditions.” That would be “a considerably tough scenario,” it says, “for equities with earnings hit hard and greater safe-haven demand for gold and the dollar.”

Why banks can live in a fantasy land in which it does not have to mark its assets to market is one of the great mysteries of contemporary finance. Christopher Whalen, the respected chairman of Whalen Global Advisors, understands how deep a hole the Fed and commercial banks have dug for themselves, i.e., the reality. MarketWatch recently summarized Whalen’s views as follows: “Now comes the more controversial part. First, he [Whalen] marks to market losses on loans and securities created during 2020 and 2021, for the impact of this year’s Fed rate hikes. That right there is enough to push banks into insolvency, with some $1.74 trillion of losses from marking to market. Another $794 billion losses comes if bank holdings of US Treasury securities, mortgage-backed securities and state and municipal securities also are marked to market. Put it all together, on Whalen’s calculations, and banks have a $1.3 trillion shortfall as of the second quarter.”

Notable Quotable

“From a technical analysis standpoint, an investor who likes to use charts as part of the tool-kit for investing and trading would be hard-pressed to find a more bullish chart set-up than the charts for gold, silver and the mining stocks. Certainly the technical picture for the precious metals sector is more than supported by several fundamental factors. It’s been well-documented that the banks have been reducing their net short-exposure to gold and silver futures contracts on the COMEX. This move has been mirrored by the BIS, the Central Bank of Central Banks, which has nearly eliminated its gold swap transactions (BIS gold swaps) after the swaps outstanding reached an all-time high in February.” – Dave Kranzler, Investment Research Dynamics

“The outcome of all this is that central banks have lost authority. At the same time, their belated policy tightening is damaging their own balance sheets because rising yields are inflicting big mark-to-market losses on the huge bond portfolios acquired since the financial crisis of 2007-09. Not all central banks will report these losses — there is considerable variation in reporting practice. Many will argue they are not profit-maximising institutions and can operate perfectly well with negative equity. They cannot go bust because they can print money.” – John Plender, Financial Times

“Gold may breach $2,000-an-ounce resistance in 2023 and never look back. This is our base case for the precious metal, notably as the Fed shifts from the highest-velocity tightening period in 40 years toward easing. A question of time is how we see gold appreciation in terms of fiat currencies and most commodities, as shown in the chart of the precious metal vs. copper. Gold has had an upper performance hand vs. the industrial metal since 2006, when the US two-year/10-year curve last recovered from an period of inversion. – Mike McGlone, Bloomberg senior macro strategist

“We have a distinctive philosophy around gold. We believe gold has unique risk/reward characteristics that enable it to help preserve real value over the long term. We use gold as a potential hedge and do not speculate on its price over the next six to 12 months. We believe it is not possible to forecast the price of gold or, for that matter, the price of other investment assets. This, in fact, is why we have a potential hedge …” – Thomas Kertsos, First Eagle Investment Management, Gold Hub interview

“We think there’s a far better yardstick [than the 60/40 portfolio]. Those of you who know us know that we’re fans of what we call a ‘cockroach portfoli’ which equally weights bonds, equities, gold and cash. By averaging exposure to all broad investment risks (inflation, deflation, long-duration and zero duration), the cockroach portfolio doesn’t depend on any particular macro regime for its returns.… Maybe it’s not just what you know that’s important in capital preservation, it’s how well you calibrate what you don’t.” – Dylan Grice, editor, Popular Delusions in a MarketNZZ interview

‘Investors have to learn that the Fed is not your friend, it’s not your pal — if anything, it’s your enemy, at least until [Chair] Jay Powell finally beats inflation.” – Jim Cramer, CNBC

“Then there are those who find this terrifyingly naïve, who believe that this year does not represent a blip, nor anything close to an ordinary business cycle. For them, the volatility in the stock markets is telling us the story of a huge structural change — one that is taking us back to a different kind of normal, one that might mean you need to forget everything you have learned about investing over the last 20 years.” – Merryn Somerset Webb, Bloomberg Opinion piece

Final Thought

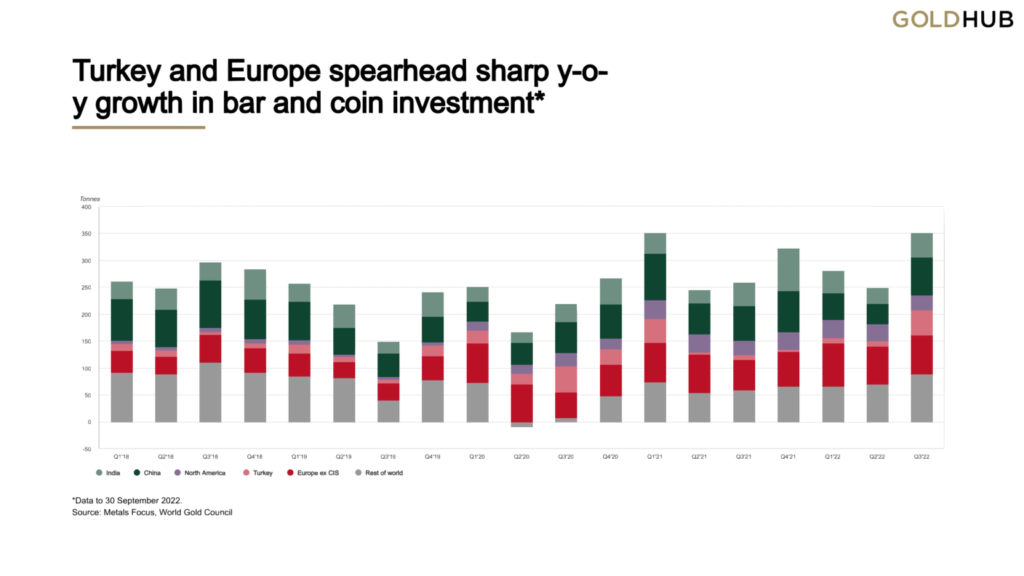

Investors worldwide rush to gold coins as hedge for the times

It is interesting to note that as economic conditions deteriorate in various economies around the world and inflation accelerates, the citizenry is turning to gold at attention-grabbing levels – an indication that the metal has not lost its standing as the favored asset of last resort.

Egyptians, reports the Middle East Eye, are “hoarding as much gold as they can” as the purchasing power of its currency plummets. In Pakistan, Bloomberg reports gold being pushed to record levels on aggressive investor buying to hedge a possible financial system breakdown.” Overall, the World Gold Council reports similarly strong demand in other emerging countries, Europe and the United States.

“Demand for gold has never been as high as this year,” says Gerhard Starsich, chief executive of the Austrian Mint. “At the moment, every gold coin that comes off the coining press has already been sold. Right now, we could sell three times as many as we are able to produce.” The Austrian Mint says it is “unable to keep up with demand as people rush to find a safe haven for their money amid surging inflation and economic fears caused by the war in Ukraine.” [Reuters/12-14-2022]

(Editor’s note: What would the chart below look like if global mints and refineries could keep up with demand?)

Chart courtesy of the World Gold Council • • • Click to enlarge

___________________________________

Are you looking for a safe haven in these highly unpredictable times?

DISCOVER THE USAGOLD DIFFERENCE

ORDER DESK:

1-800-869-5115 x100 • • • orderdesk@usagold.com • • • ORDER GOLD & SILVER ONLINE 24-7

–––––––––––––––––––––––––––––––

The six keys to successful gold ownership

This eye-opening, in-depth introduction to precious metals ownership will help you avoid many of the pitfalls that befall first-time investors. Find out who invests in gold, what role gold plays in serious investors’ portfolios, and the when, where, why, and how of adding precious metals to your holdings. To end right, it is critical that you start right, and the six keys to successful gold ownership will point you in the right direction.

–––––––––––––––––––––––––––––––

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such, USAGOLD does not warrant or guarantee the accuracy, timeliness, or completeness of the information found here. The views and opinions expressed at USAGOLD are those of the authors and do not necessarily reflect the official policy or position of USAGOLD. Any content provided by our bloggers or authors is solely their opinion and is not intended to malign any religion, ethnic group, club, organization, company, individual, or anyone or anything.

–––––––––––––––––––––––––––––––––

Michael J. Kosares is the founder of USAGOLD, author of The ABCs of Gold Investing – How To Protect and Build Your Wealth With Gold [Three Editions], and the firm’s publications editor.

Michael J. Kosares is the founder of USAGOLD, author of The ABCs of Gold Investing – How To Protect and Build Your Wealth With Gold [Three Editions], and the firm’s publications editor.

About the author

Michael J. Kosares is the founder of USAGOLD and the author of The ABCs of Gold Investing – How to Protect and Build Your Wealth With Gold. He is also editor and commentator for USAGOLD’s Live Daily Newsletter and editor of the News & Views monthly newsletter.

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. The utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD does not warrant or guarantee the accuracy, timeliness, or completeness of the information found here. The views and opinions expressed at USAGOLD are those of the authors and do not necessarily reflect the official policy or position of USAGOLD. Any content provided by our bloggers or authors is solely their opinion and is not intended to malign any religion, ethnic group, club, organization, company, individual, or anyone or anything.

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. The utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD does not warrant or guarantee the accuracy, timeliness, or completeness of the information found here. The views and opinions expressed at USAGOLD are those of the authors and do not necessarily reflect the official policy or position of USAGOLD. Any content provided by our bloggers or authors is solely their opinion and is not intended to malign any religion, ethnic group, club, organization, company, individual, or anyone or anything.